Economic Chaos or Opportunity?

Economic Chaos or Opportunity? History Repeats Itself — Which Path Do We Choose?

“A smooth sea never made a skilled sailor.” – Franklin D. Roosevelt

We’ve seen this before. Markets rise and fall. Rates soar, then crash. Governments overspend, consumers overborrow, inflation bites — and then, somehow, we bounce back stronger.

Right now, the economy feels like a boat tossed on unpredictable seas. Between higher interest rates, stubborn inflation, and growing uncertainty, it’s easy to feel adrift. But the truth? We’ve been here before. And we’ve come out ahead — every time, economic Chaos or Opportunity?

The Optimist’s View: Set Your Sails — The Wind Will Change

Let’s talk about what we’re seeing — and why it’s not all doom and gloom.

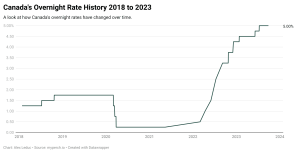

Interest Rates: They’ve Peaked Before, and Then Dropped

-

In 2008, the Bank of Canada cut rates by 2.5% in one year.

-

In 2020? A 1.5% drop in less than 12 months.

-

From May 2024 to June 2025: another 2.25% drop already underway. Pattern? Rates rise fast, then fall fast. Always have. History suggests we’re halfway through this rate cycle.

Real Estate: Prices Are Holding, and Equity Is Plentiful

-

Vancouver Island’s home prices are only 1.7% below 2022’s peak.

-

Anyone who bought in 2020? They’ve gained nearly 60% in home value.

-

Plenty of equity means refinance opportunities are still alive, especially after the first rate cut in June 2024.

For buyers who missed the 2021–2022 boom: your time might just be now.

Employment & Growth: We’ve Bounced Back Before

-

Yes, unemployment is up slightly.

-

Yes, consumers are cautious.

-

But Canadian inflation is back near target (1.7%) and wages are still rising.

In past recessions — like in the early 1980s, the 2008 financial crisis, or COVID’s 2020 chaos — we saw stronger growth emerge after periods of belt-tightening.

Tariffs, Debt & Deficits? Been There, Done That

In the 1930s, the Smoot-Hawley Tariff Act sparked a global downturn. Today, tariffs are still making noise, but we’re also:

-

Far more globally integrated

-

Faster to respond with policy

-

Quicker to innovate our way through disruption

And yes — even Warren Buffett said Trump’s tariffs are “a tax on goods.” But as with all taxes, we adapt.

The Other Side: What Happens if the Elephant Sneezes?

But let’s not sugarcoat it. When the U.S. sneezes, Canada doesn’t just catch a cold. Sometimes we get pneumonia.

Signs of Trouble:

-

U.S. job losses and jobless claims rising again

-

Consumer sentiment lowest in 12 years

-

Deficits soaring: $1.83 trillion, and counting

-

Tariff wars and political unrest mounting

If the U.S. economy staggers into full-blown stagflation — high inflation + low growth — it won’t just be a sneeze. It’ll be a stampede.

What That Could Mean for Us:

-

Canadian exports fall (we sell 75% to the U.S.)

-

Our bond yields rise if U.S. debt causes panic

-

Fixed mortgage rates could stay high even if BoC cuts

-

Investor confidence erodes if U.S. markets spiral

So, What Do We Do?

The “Set Your Sails” Strategy

-

Refinance if you can. Use your home equity. Rates are falling — timing matters.

-

Buy smart. Home prices have corrected slightly. With long-term amortizations, monthly payments are within reach again.

-

Stay diversified. Markets will rebound. Real estate, balanced investments, and steady income matter more than chasing hot trends.

The “Elephant Sneezes” Contingency

-

Build emergency savings.

-

Lock in fixed rates if you’re unsure about the future.

-

Don’t overextend on credit. U.S. bankruptcies and credit write-offs are flashing warning signs.

Final Thought: History Doesn’t Repeat — But It Rhymes

Every cycle brings fear — and eventually, recovery.

The 1980s. The Dot-Com bust. The 2008 collapse. COVID. Now 2025.

We’ve seen the storm clouds before. What sets winners apart is not fear or panic — it’s preparation, patience, and perspective.

So whether you see the wind shifting in your favor or hear the elephant sneeze in the distance, know this:

The tide always turns. The question is: Will you be ready to sail when it does?

Blog Posts

Insured Mortgage Changes

BC Tenancy and First Time Buyers

Zoning Changes: City of Nanaimo Bill 44 Response

Maximizing Income vrs Using Business Write Offs

Mortgage News

BOC Cut = lower interest costs

.jpg)