Understanding Fixed vs Variable Mortgage Rates in BC

When choosing a mortgage, one of the biggest decisions you’ll make is whether to go with a fixed rate or a variable rate.

It’s also one of the most misunderstood.

Many buyers automatically lean toward fixed rates for stability, but does that always make it the better option? Let’s break down the differences, look at historical trends, and help you understand what might work best for your situation.

What’s the Difference Between Fixed and Variable Rates?

Fixed Rate Mortgage

A fixed rate means:

- Your interest rate stays the same for your entire term

- Your payments are predictable

- You’re protected from rate increases

This option is often chosen for peace of mind and stability.

Variable Rate Mortgage

A variable rate means:

- Your rate can move up or down over time

- It’s influenced by the Bank of Canada and lender prime rates

- You may benefit if rates decrease

Some variable mortgages also have fixed payments, where only the portion going toward interest vs. principal changes.

Understanding the Risk (and Reward)

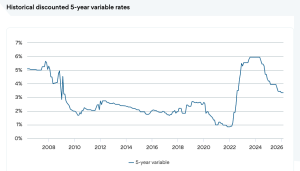

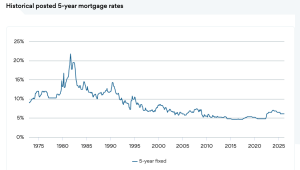

One of the best ways to understand risk is to look at what’s happened historically.

Looking at historical variable rates, we can see that while they do fluctuate, they’ve generally remained within a relatively moderate range.

- Highest: ~5.94%

- Lowest: ~0.90%

Now comparing that to fixed rates over time:

- Highest: ~5.69% (in recent cycles)

- Lowest: ~1.39

What This Actually Shows

While variable rates do move more frequently, the difference in extremes isn’t as dramatic as many people expect.

- The highest variable rate was only about 0.25% higher than fixed

- The lowest variable rate was actually lower than fixed by ~0.49%

In other words: Variable rates come with movement, but not necessarily extreme unpredictability AND can save you money in times where the interest rate has dropped.

Why Variable Rates Get a Bad Reputation

A lot of the hesitation around variable rates comes from recent rate increases. When rates rise quickly, it’s natural to want certainty (and fixed rates provide that.)

But historically:

- Variable rates have often performed well over time

- They’ve offered potential savings in many market cycles

That doesn’t make them “better,” just different.

Pros of Fixed vs. Variable

Fixed Rate Pros

✔ Predictable payments

✔ Protection from rate increases

✔ Easier budgeting

Variable Rate Pros

✔ Potential for long-term interest savings

✔ Lower penalties if you break your mortgage early

✔ Ability to benefit when rates decrease

✔ Often more flexibility

So… Which One Is Better?

There’s no one-size-fits-all answer.

It comes down to:

- Your comfort with change

- Your financial goals

- Your timeline

- Your overall situation

Some people value stability above all else. Others are comfortable with some fluctuation in exchange for flexibility and potential savings.

Let’s Talk About What Works for You

If you’re unsure which option makes sense for your situation, that’s exactly what we’re here for.

We’ll walk you through the numbers, explain the trade-offs, and help you make a decision you feel confident about.

Reach out anytime to start the conversation.